Ledger-native settlement

Payment settles straight to the operator on the XRP Ledger, tied back to the exact machine and sale.

Programmable payment terminals built for automated retail and unattended vending. Accept supported payment methods with direct, on-chain settlement.

Payments only get cheaper when both sides run on the same rail. The customer side has had a decade of investment. The machine that takes the payment has not.

Cards, mobile wallets, and tap-to-pay made checkout effortless for the customer. A digital-asset card even looks like paying on-chain.

At the machine, that payment still runs the card networks. Interchange and processing fees apply in full, and the digital asset is converted to fiat before the operator ever sees it.

Terminuity rebuilds the machine-side hardware so payment can settle straight to the operator on the XRP Ledger, on a terminal that drops into the equipment they already run.

Terminuity delivers an end-to-end experience. By deploying our software directly into the terminal and layering blockchain-native rewards on top, we turn separate components into one unified ecosystem.

The software company and the parent. Terminuity designs and ships the hardware line, the operating system, and the rewards layer.

The device category. A FinTerminal is a programmable, ledger-native payment terminal. It names the class of device, the way “point of sale” names a class, not a single model.

The hardware. Vendrive builds the terminals operators install on their machines, from a unit that retrofits an existing machine to a full vending machine built around the same terminal.

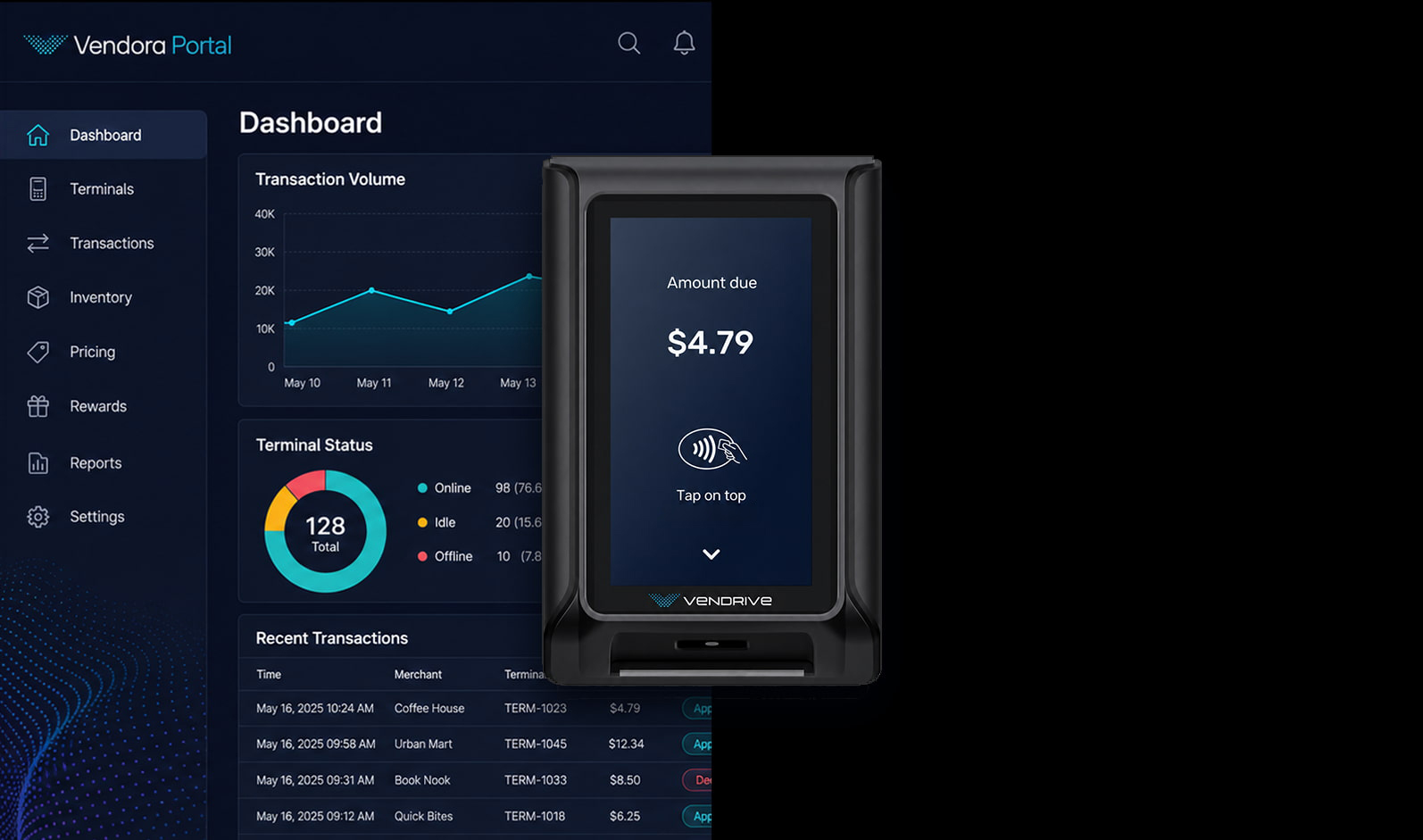

The operating system. Vendora OS runs on every Vendrive unit and powers the operator portal. Inventory, telemetry, pricing, alerts, and reporting run in one place.

The rewards layer. Vendpass attaches loyalty to the payment card itself. No account, no email, no app. The card earns and redeems at the terminal.

Unattended hardware requires an intelligent edge. Terminuity replaces fragmented legacy add-ons with a unified terminal layer that secures the sale, tracks the asset, and synchronizes the entire ecosystem.

Vending, smart coolers, EV charging sites, alongside managed residential amenities, hospitality spaces, gyms, and other member environments.

Consolidate payment, telemetry, inventory, and on-screen advertising into a single terminal. Manage inventory, rewards, AI dynamic pricing, and more from one unified layer.

Every transaction, telemetry pulse, and inventory shift routes instantly from the physical terminal to the operator portal, keeping up-to-date at all times.

A card payment passes through a chain of intermediaries before the operator is paid, and each one takes a cut and adds delay. A wallet payment on Terminuity settles on the XRP Ledger and lands with the operator directly, with no acquirer, processor, or network in the middle.

Tap, swipe, or insert at the machine.

Reads the card, encrypts, hands off.

Routes to the acquirer and takes a fee.

Visa, Mastercard, or Amex authorizes.

The machine releases the product.

Funds clear over the following days.1–3 days

Taps to pay or scans the request, signs on their phone.

The terminal watches the ledger for the matching payment.

The payment validates on the XRP Ledger.Seconds to finality

The terminal signals the machine to release.

Held on-chain, or moved to a bank through a fiat off-ramp.On-chain instantly

Why it matters: The cost of a traditional card transaction is driven entirely by legacy intermediaries. By settling directly on-chain, Terminuity allows operators to retain significantly higher unit margins while unlocking highly scalable transaction routing and software fee layers for Terminuity.

Stablecoins keep the price steady today. As the rails mature, the terminal is designed to widen what it can accept and how operators get paid.

Stablecoins anchor the experience now. Support for a wider set of supported wallets and assets is designed to follow as liquidity and coverage allow.

Accepting assets that move in price, always quoted against a fair, current market rate via Chainlink Runtime Environment (CRE).

Where regulation and off-ramp partners allow, operators will be able to choose how they hold and withdraw what they earn.

Terminuity starts with the machines operators already run. The same terminal architecture scales from a retrofit unit to a full machine built around the system.

A plug-and-play terminal for existing MDB-compatible vending and automated retail equipment. It brings payment, cellular connectivity, telemetry, and Vendora OS to the machine without replacing the cabinet.

The same terminal architecture scales into screen-based units, custom installations, and full Vendrive machines built around the system from the start.

Legacy hardware took a payment and triggered a vend. Vendora OS runs the whole machine and the fleet behind it, so an operator manages inventory, pricing, alerts, and rewards from the same place the payment happens.

Loyalty at a machine usually dies at the friction. Nobody downloads an app or types an email to save a few cents on a drink. Vendpass attaches the rewards to the payment card itself, so the first tap already counts.

Built for staffed stores and bolted onto machines that were never meant for it.

The payment card the customer already tapped becomes the loyalty account, automatically.

Wallets and exchanges now issue a virtual card that pays from a digital-asset balance over the same contactless hardware as any card. Paying on-chain is becoming a tap. Terminuity is built for that first, and keeps cards and QR working right alongside it.

Tap a digital-asset balance through a virtual card on standard contactless, and the terminal settles it on the ledger. When a tap is not available, the customer scans the on-screen request and approves from a wallet. Same settlement, reached a different way.

Terminuity does not rebuild card processing. It runs on pre-certified reader modules and established gateway partners, so every customer who still reaches for a card pays exactly as they do today while the ledger rail grows underneath.

The terminal that brings ledger-native settlement to the machines operators already run. It connects through the standard MDB port, runs Vendora OS, and takes payment by contactless tap or scan-to-pay.

Where the terminal stops being an add-on and becomes the machine. These are early design concepts for the full Vendrive unit, built around the terminal from the start.

A vending screen sits dark most of the day. Between sales, Terminuity fills it with promotions and local advertising, turning the most-passed surface in the building into something that earns.

Operator promotions, local advertising, and rewards messaging run while no one is at the machine, on a surface that already has foot traffic.

The moment a customer steps up, the ad drops away and the screen is back to the purchase. Selling always wins over showing.

On a one or two dollar sale, the fixed slice of a card fee eats most of the margin, and it never shrinks with the ticket. Settling on the ledger removes the layers that fee pays for, on a terminal that drops into the equipment already on the floor.

Ledger settlement skips the interchange and gateway layers. The smaller the ticket, the more that saving matters.

The ledger reaches finality in seconds, against the multi-day wait of card settlement.

The terminal retrofits existing machines through the MDB port, and cards keep working the whole way through.

The idle screen runs ads between customers, adding revenue the machine never had before.

Terminuity integrates directly with the infrastructure operators already rely on. We don't ask the market to change its habits; we upgrade the plumbing underneath.

Customers continue using the payment methods they already trust. Card processing and traditional mobile wallets run securely through certified hardware modules and established payment gateways.

Merchants gain an independent, low-cost transaction rail that routes supported digital wallet payments directly to their account with near-instant finality.

FinTerminals are engineered with a plug-and-play architecture designed for frictionless, market-by-market deployment. Our software stack adapts dynamically to the unique regulatory environments, dominant stablecoins, and compliant payment rails of each target market.

Our architecture is designed to use certified card hardware, regulated payment partners, and supported digital-asset settlement infrastructure.

Terminuity will execute localized compliance audits before activating advanced capabilities. Card acceptance, digital-asset settlement routing, stablecoin compatibility, and regional fiat off-ramp coverage will undergo exhaustive partner and legal review on a market-by-market basis. This applies across all standardized retail deployments as well as specialized, controlled member environments; including but not limited to, EV charging sites, retail hospitality, or residential amenities.